⚛️ Uranium: Fueling the Energy Comeback

The Uranium Convexity Trade

🧭 Executive Summary

We believe uranium is in the early stages of a multiyear structural bull market, driven by:

A global nuclear resurgence

Tightness across the entire fuel cycle

Government-led investment and policy tailwinds

A supply response that remains slow and highly concentrated

Utilities are locking in long-term contracts. Governments are stockpiling. And enrichment capacity - especially in the West - remains deeply inadequate.

This is one of the most asymmetric energy setups on the planet.

🌍 Macro Context: The Policy Flywheel

The U.S. Department of Energy (DOE) is directly funding enrichment and contracting domestic uranium supply through multibillion-dollar DPA and IRA programs.

The ban on Russian uranium imports is now law - with no waivers permitted after 2027.

SMRs are in motion: DOE reopened a $900M funding program for reactor builds and supply chain development.

International allies (UK, Canada, France, Japan) have formed the Sapporo Five, pledging >$4B toward enrichment and SMR deployment.

Utility contracting is accelerating, while spot market activity remains thin - a sign of rising off-market strategic demand.

This is no longer a speculative trade. It’s a national security realignment.

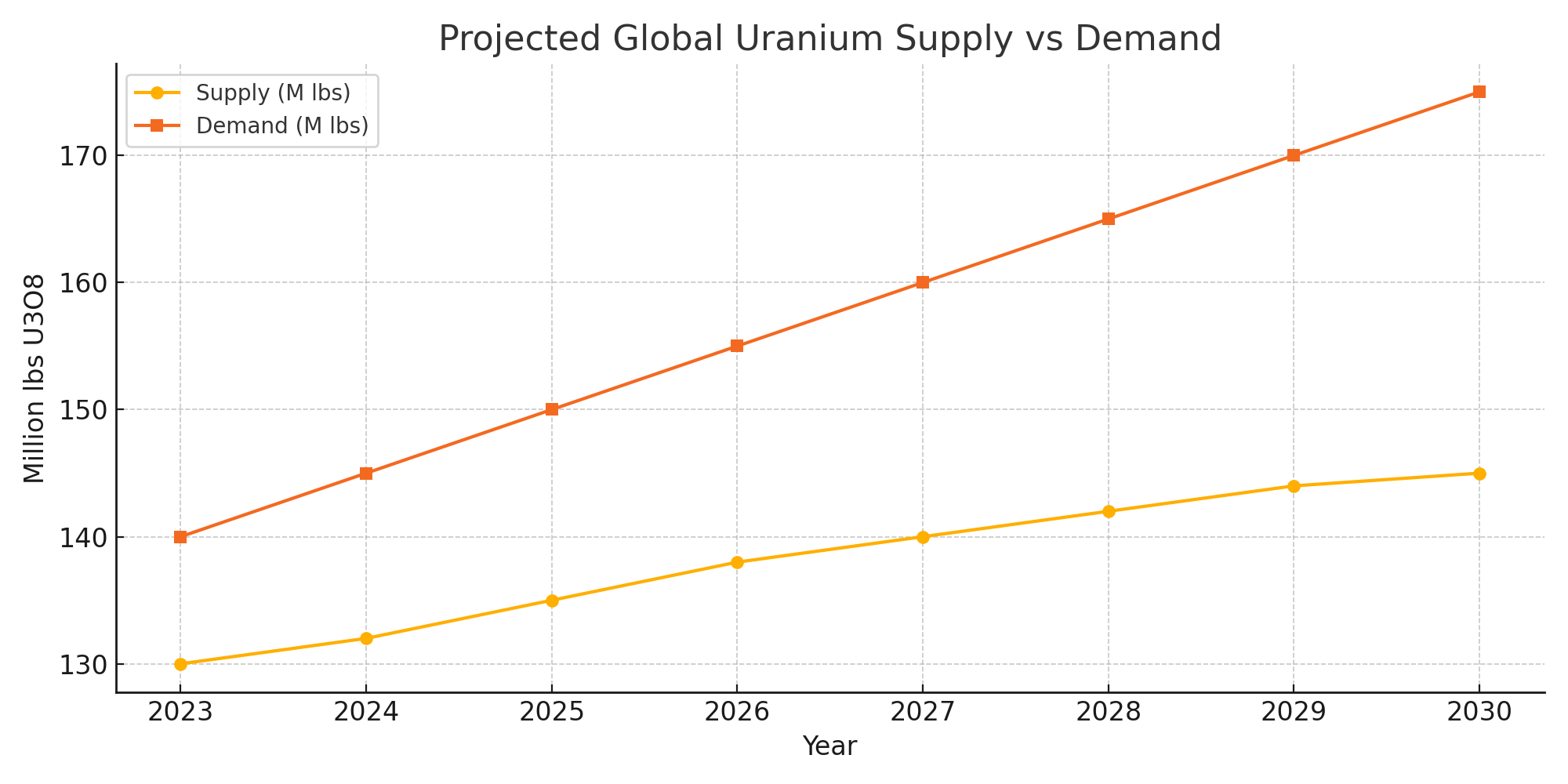

⚛️ Fuel Cycle Breakdown: Tight All the Way Down

Demand:

60+ nuclear reactors under construction globally

U.S. SMR pilot projects receiving DOE subsidies

Life extensions approved across U.S., Canada, France, and South Korea

Supply:

Only a few producers dominate: Cameco, Kazatomprom, and select juniors

Enrichment capacity is maxed out - especially with Russia off the table

Conversion bottlenecks are just as severe as raw uranium shortages

🔎 Critical Fact:

The DOE has confirmed Russia still supplies ~44% of global enrichment. With U.S. imports banned post-2027, that capacity must be rebuilt domestically.

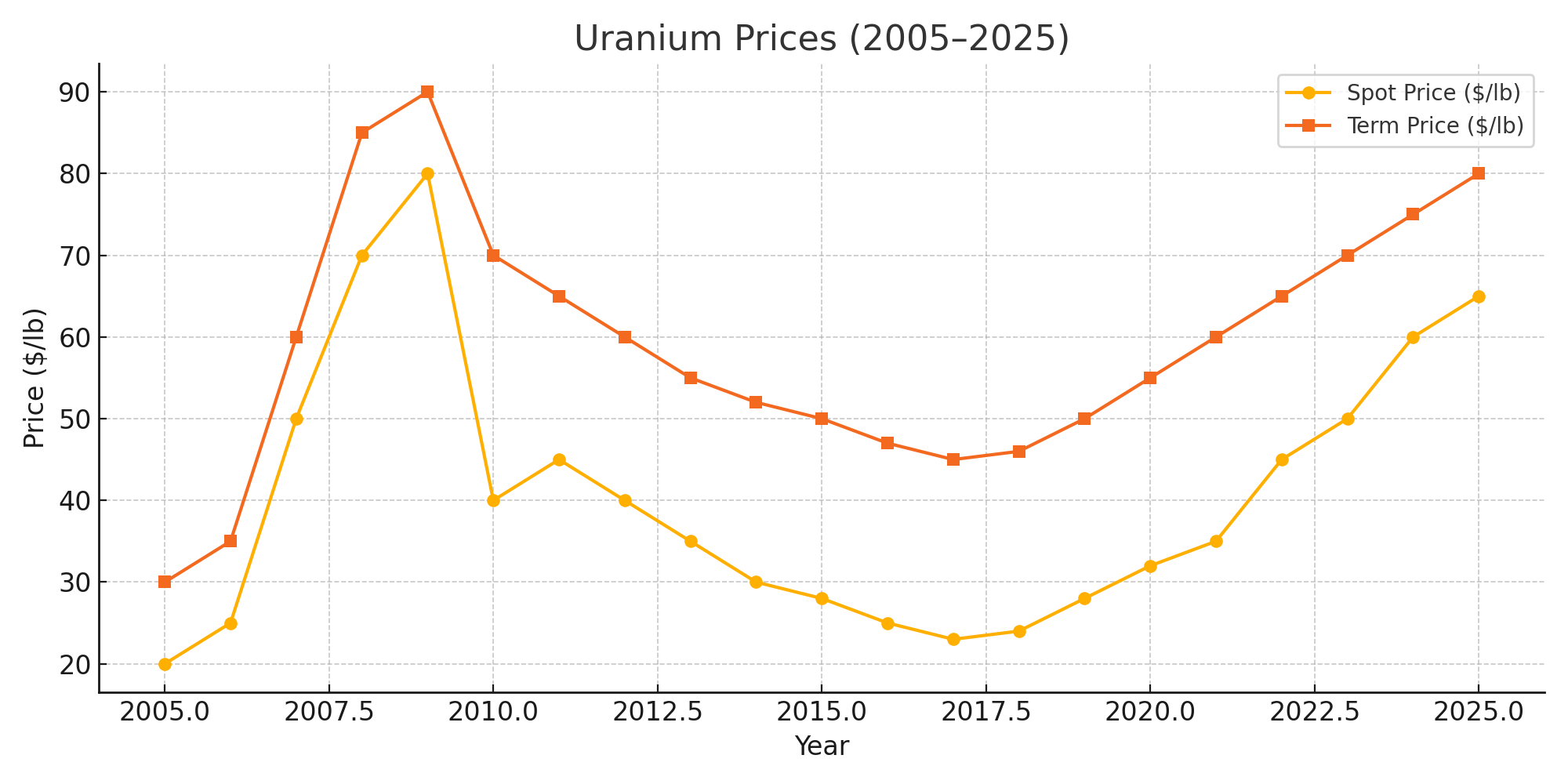

📈 Catalysts

✅ U.S. ban on Russian uranium fully passed - no waivers allowed after 2027

✅ Centrus, Urenco, and Orano now funded by DOE to ramp domestic enrichment

✅ DOE $900M SMR pilot program reopened in April 2025 - selecting new sites

✅ NRC SMR licensing: NuScale approved, X-energy in active review

✅ ETF flows rebounding: URNM gaining capital, even as Sprott Physical sees volatility

✅ Spot uranium rebounding: ~$71–75/lb (U3O8), while term prices continue rising

⚠️ Risks

Reversal in nuclear sentiment or policy shifts in OECD markets

SMR buildout delays or permitting friction

Speculative junior dilution / execution risk

Volatility from macro flows (rates, liquidity) affecting short-term ETF demand

📦 Positioning Framework

🔋 Core Exposure

Cameco (CCJ) – Tier 1 production + conversion optionality

URA / URNM – Diversified equity baskets (exploration to production)

SRUUF – Sprott Physical Uranium Trust (spot exposure)

Juniors – NXE, DNN, UEC, DML.TO - leverage to contracting cycle

⚙️ Options-Based Structures

LEAPS on URNM or CCJ (Jan 2027+)

Call spreads or synthetics to express long convexity with risk controls

LEAPS + overwriting to enhance yield and reduce carry cost

📐 Capital Efficiency Matters

Not all uranium exposure is created equal.

Cameco offers rare capital discipline: long-life Tier 1 assets, integrated conversion, and clean FCF yield. At ~$75/lb spot uranium, ROIC already exceeds WACC - and term prices suggest more to come.

Juniors, on the other hand, often burn cash. But a few offer genuine leverage to pricing and contracting cycles - if positioned carefully.

This is a classic Potato Capital setup: core capital-efficient exposure + risk-sized convex optionality.

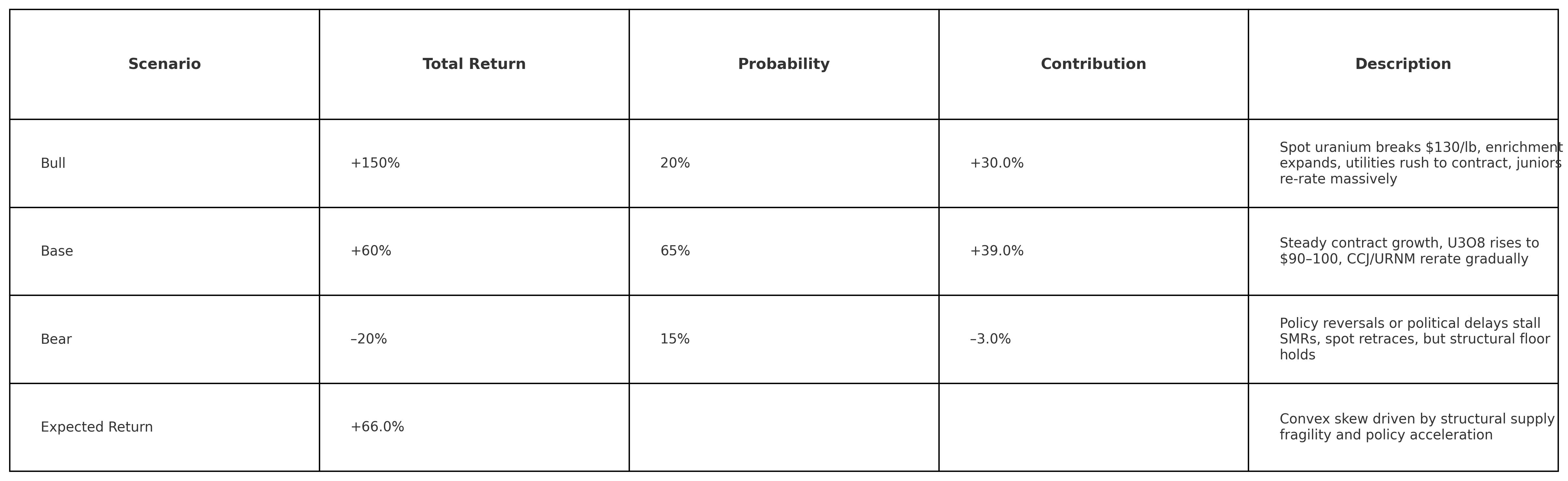

📊 Scenario Framework

The distribution here is intentionally convex.

The bull case isn’t the most likely outcome - but it is plausible, underpriced, and highly impactful. That’s where structural asymmetry lives.

The base case reflects gradual but durable tailwinds: government contracting, policy insulation, and term price normalization.

The bear case is cushioned by strategic stockpiles and long-term demand - so the downside isn’t zero, but it's tolerable.

With an expected return of ~66%, we believe this is a uniquely structured trade where the market is still mispricing the range of credible outcomes.

This is exactly the kind of thesis we look for:

Macro-aware: Government policy, supply chains, and geopolitics are driving outcomes

Capital-efficient: Tier 1 producers can convert higher prices into FCF with minimal capex

Convex: The upside is nonlinear - while the downside is cushioned by term demand and policy anchors

Under Owned: Institutional flows are building, but broad portfolios remain underexposed

We’re not chasing momentum. We’re modeling asymmetry - and positioning where others aren’t looking.